Department reminds consumers to focus on the basics of financial planning

NASHVILLE – As many Tennesseans begin resuming their regular work, recreation and spending habits, the Tennessee Department of Commerce & Insurance’s (TDCI) Division of Regulatory Boards reminds consumers to use the post-pandemic economic landscape to focus on improving their financial literacy and awareness.

A simple thing such as a household budget can help Tennessee families achieve their short- and long-term financial goals.

TDCI oversees the licensure of credit and debt collection professionals through the Collection Service Board, Debt Management Program and the Credit Services Business registration program.

“The pandemic saw the finances of Tennesseans from all walks of life dramatically altered,” said TDCI Executive Director Roxana Gumucio. “As we move forward, I want Tennesseans to remember that the basics of financial planning, such as creating a household budget, can help them reach their financial goals.”

As part of the series of consumer financial tips, TDCI emphasizes that creating and using a written budget can help families move forward in achieving their financial goals.

Here’s a refresher on some of the basics that could help you in the long run:

- A budget needs to be in writing to be effective. Complicated financial software or an expensive budget book might be intimidating or too pricey for some. If so, start with a simple spreadsheet or a sheet of paper with columns. Regardless of the format, choose what you will be most likely to use consistently.

- Build a budget. Create a template with columns for the bills or expense, the due date, the amount and then each month of the year to track the amount paid as there are some payments that may vary depending on the time of the year, especially utilities.

- Involve everyone. If your budget is for a household, make sure you involve everyone in the planning and tracking. If one party is very strict in following the budget and the other does not follow the budget this can create financial and relationship issues. Agree at the beginning, compromise and come up with a plan that all can agree on and follow.

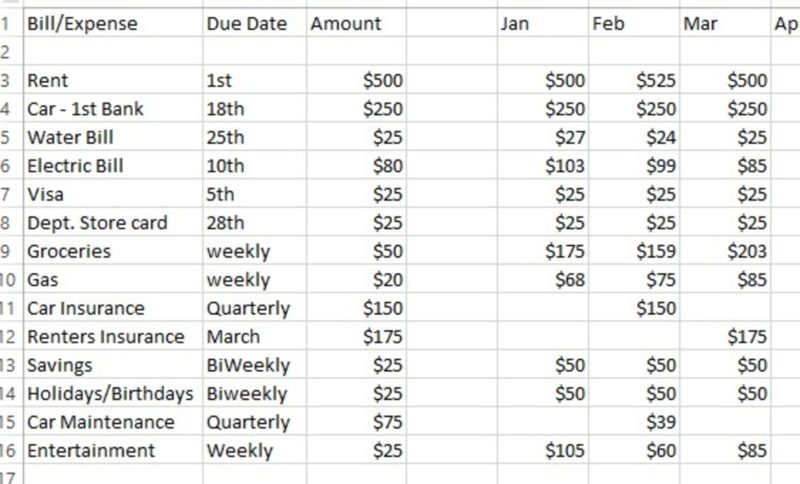

- Make sure your budget is complete. List all your bills (rent, car payment, utilities, etc.) and expenses (groceries, gas, car maintenance, subscriptions, etc.). Do not forget to include things like birthday gifts, holiday expenses, entertainment and other extras as those things can add up. If a bill or expense does not have a specific reoccurring due date, list it as weekly, monthly, quarterly or annually, as appropriate. Your final budget might look something like this:

- Once the budget is complete, compare it to your income. If you have income left over determine where it can be best used to further your financial goals. Do you want to save more or pay off some bills sooner? Or maybe you cut corners on entertainment or holidays in your initial plan, and you want to increase those amounts. There is nothing wrong with having a cushion in your budget for unexpected expenses either. (If you do not already have a savings account or emergency fund, be sure to add this to your budget. You can do this by having an amount direct deposited into a separate savings account. If you don’t have direct deposit, transfer funds first when you are paid. You may not be able to put a large amount in this account at first, but it is important to start it even if the amount is minimal. As your budget improves, you can increase the amount. Set a goal to have three (3) to six (6) months of bills and expenses covered with this fund.

- Make some cuts. If you fall short when you compare your budget to your income, then it is time to search for ways to cut expenses or generate more income. Can you reduce your unnecessary expenses? For example, you should comparison shop for lower insurance rates, cell phone plans or cable packages to see if you have the best deal.

- Stick with it! It will be tempting to quit tracking your budget as your financial situation improves (or to get off budget and spend extra money). When the temptation comes, stop and think about your financial goals. Being debt-free, saving for the down payment on a home or higher education requires taking steps today. Making wise decisions now can help you in the long run.

{kind=link}